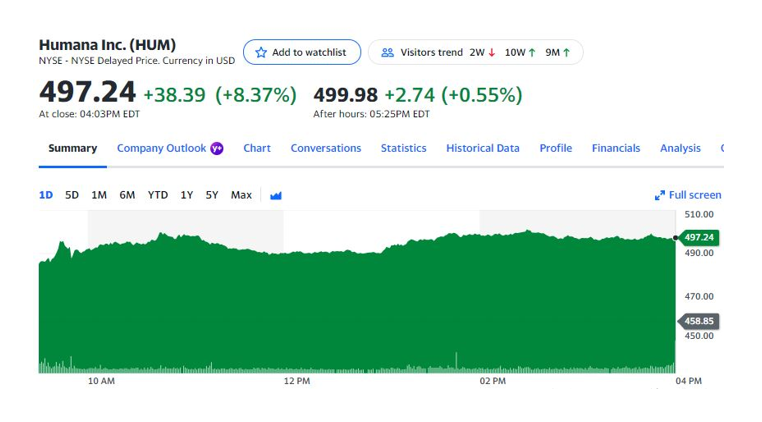

September 16, 2022 – The first headline reads: “The insurer [Humana] also raised its profit outlook for 2022, sending its shares up some 8% since the news Thursday.”[1] Yet, another headline read: “FedEx Stock Hits Two-Year-Plus Low After ‘Ugly Quarter And Outlook.’”[2] That was the takeaway on what ended one of the more difficult weeks for U.S. stock values.

On the Humana side, they raised guidance and predicted a 14% annualized growth rate in earnings per share above their last projections. The company downplayed any material impact from COVID going forward, and they projected continued growth in Medicare Advantage membership. Medicare Advantage is the private insurer side of the U.S. government program for those over the age 65. We have projected this to be a guaranteed growth for the rest of this decade. “Humana’s total MA [Medicare Advantage] enrollment rose 5.2% to 5.1 million by the end of the first quarter. That membership includes 4.5 million enrolled in individual MA plans.”

Humana also noted, “”With the investments we’ve made for 2023, we believe strongly in our ability to continue to grow at or above industry growth for the long run,” Broussard said. “We have consistently grown faster than the industry, due mainly to our differentiated Medicare Advantage capabilities. We responded quickly to our disappointing 2022 MA results by making meaningful adjustments to our product offering segmentation, distribution and marketing for 2023.”

Humana’s stock took off on this news release.

On the other hand, Federal Express had a challenging day. First, according to CNBC[3] their CEO was quoted as saying they expected a “worldwide recession,” this was after they reported lower revenues than expected. This appears to have frightened investors as shares were down as low 19% from the previous close. The company announced it was parking planes, closing offices, and other actions to adjust volume and cost in part by freezing hires. The situation was so sudden and concerning that the company withdrew all forward-looking guidance.[4]

What is our point here?

For years, particularly since the COVID pandemic started, we have noted that the most stable industry in America was not technology, social media platforms, Finance or even FinTech in general, it is healthcare. We see nothing that will stop or slow the continued growth of healthcare cost for the rest of this decade if we remain on the current path. While there is great interest and talk about reducing cost and in improving quality, our position in this industry continues to remain the same – with the proper use of existing and emerging technology, we can and must achieve both! However, the old idiom rings ever true in this case: “when everything is SAID and DONE, there is much more SAID than DONE!”

With healthcare leading the largest segment of U.S. GDP, the problems are becoming progressively worse for the industry; however, increasingly better for the healthcare investor. I was one of those that thought COVID would hit healthcare companies a with higher cost and utilization rate however, I was wrong. What I did not foresee though was “inflation” could have such substantial and broad impact. In this case, if not the main, the best opportunity to control rising “infrastructure” costs (brick and mortar, labor, and expenses) versus utilization cost is with more efficient systems and much better of use of technology. Therefore, without reservation, we believe that new systems and better use of technology in healthcare assures a very bright future for those ahead of the curve.

-Noel J. Guillama, Chairman

[1] https://www.fiercehealthcare.com/payers/humana-looks-regain-its-footing-medicare-advantage-market-raises-profit-outlook

[2] https://www.investors.com/news/fedex-stock-dives-delivery-giant-pulls-earnings-guidance/

[3] https://www.cnbc.com/2022/09/15/fedex-ceo-says-he-expects-the-economy-to-enter-a-worldwide-recession.html

[4]https://www.wsj.com/articles/fedex-says-preliminary-first-quarter-results-miss-expectations-as-macro-trends-worsen-11663275276