In our last two blogs, we focused our attention on discussing the growth and size of the Medicare Advantage program. Recently, a major Wall Street financial firm found the addressable market size was over $325 billion per year and the growth rate for the last 15 years has been quite impressive; however, we believe we are nowhere near the peak for the program. The title of these blogs betrays our horizon at 14 years, a point at which we think the market will stabilize as Generation X enters Medicare.

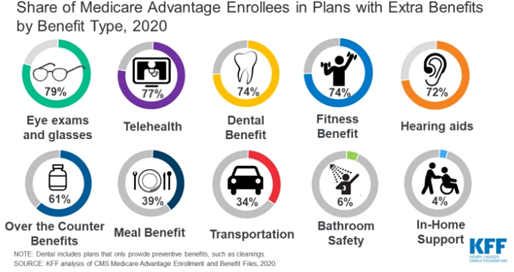

Medicare Advantage offers a degree of financial security over their healthcare expenditures to retired seniors. Over 60 percent of all Medicare Advantage plans have no premium, and as we noted before, in some hot markets, the entire Medicare Part B cost (approximately $150 per month) is reimbursed to the beneficiary. The reality is that in all cases, Medicare Advantage offers more coverage than traditional Medicare. Below is an excellent visualization by the Kaiser Family Foundation.

Medicare Advantage has always provided financial security for those seniors on a budget. As a healthcare operator, we have contracted over a dozen occasions to provide medical care coordination and medical services to managed care/insurance companies. However, my point of reference for my confidence in the system is that both of my parents have been part of one of the top providers (graphic displayed below), and both have had very positive experiences and benefited financial security from the program. I would argue both had better care because they had a company with a vested interest in their continued good health. That is topic for a future blog.

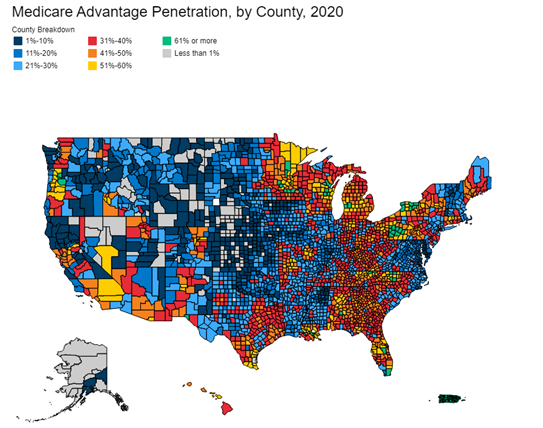

As you can see from the color map below, the highest Medicare Advantage penetration (red, yellow, and green) has been in the Southeast (USA), and in particular, our home state of Florida, neighboring Georgia, Alabama and big part of South Carolina. Also, the Entire Appalachian and Allegany Mountain ranges, from Georgia to Pennsylvania. You also can add nearly all of Ohio, Michigan, Wisconsin, and Minnesota (home of United Healthcare). Loss of penetration in part of Washington State, New York and the Midwest including concentrated parts of California.

As noted in the graphic, the U.S. Government actuaries project national penetration above 51% by 2030, we are very confident that the numbers will be much higher, as more companies compete with more services, and even more technology. Medicare Advantage has finally become a mass appeal consumer product/service for all those approaching 65, or still part of traditional Medicare.

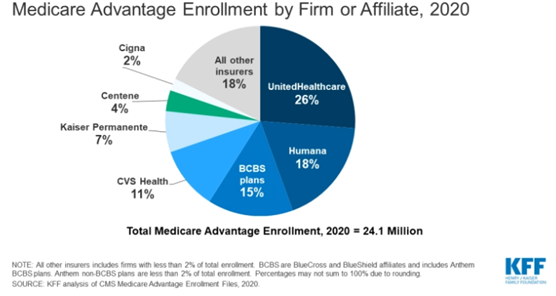

The largest company in the Medicare Advantage space is UnitedHealthcare. That is not only impressive, but you must know that they also operate the largest independent medical service organization (Optum) at over $10 billion in annual medical revenues, and recently purchased one the premier healthcare data intermediaries in the country processing billions of medical transactions. They seem to predict that the future of healthcare is consumer based, tech driven (not enabled) and that you must provide the care to control the quality and cost. Being the second largest program in size, Humana has interestingly had many interactions, as well as provided care via their Conviva medical group.

It should be obvious that the future of Medicare Advantage is not only very bright, but also the days of traditional fee-for-service Medicare are numbered, and we believe it will phase out in the next few years. This will have an impact on all the other parts of medical care, from commercial insurance to Medicaid.

We believe that the future is bright and will continue to grow brighter as more companies begin to see the solid future in Medicare Advantage, from the ‘baked in’ 6%+ CAGR solidified by the 10,000 persons (on average) turning 65 daily from now through 2030, and become eligible for Medicare, of which more than 51% will choose a Medicare Advantage Plan.

-Noel J. Guillama, Chairman